Most major banks in Namibia include a travel insurance benefit when a qualifying credit card is used to purchase a return international flight.

While this is a great value-add, the cover can be limited and may not provide complete protection when travelling abroad.

“Credit card travel insurance offers a cost-effective way to access a basic level of protection when you travel. But, knowing its limits is crucial,” says Franco Feris Chief Executive Officer at Santam Namibia Limited.

“Travellers must understand what is and isn’t covered before leaving the country to avoid any unwanted surprises while abroad,” says Feris.

He explains that the cover offered with credit cards typically provides a level of emergency medical assistance for short trips, basic benefits to meet visa requirements, limited protection for healthy travellers and optional top-up cover for added benefits.

Risks emerging from situations such as trip disruptions, adventure activities, long travel, or pre-existing medical conditions are not usually covered.

Feris adds that travellers using credit card insurance must consider finer requirements such as purchasing the flight on the qualifying card, manually activating the cover online or via phone, and confirming that the card tier qualifies (i.e. gold, platinum, or black).

Even when activated correctly, there are some gaps in cover. Feris advises travellers to be aware of things such as that medical cover is limited.

“Emergency coverage limits are smaller than standalone policies,” he says.

“Claims can be denied for alcohol, drugs, reckless behaviour, or motorcycling without a license. This can be especially risky given medical inflation and the high cost of treatment abroad.”

There is also age and trip length limits to any cover.

“Many credit card related policies may exclude travellers over age 70 and limit trips to between 30 and 90 days. Longer trips often require a top-up.

“Adventure activities are typically excluded,” he says. “Skiing, surfing, bungee jumping, scuba diving, and quad biking are often excluded. Special add-ons might be necessary.”

Even work injuries are not covered. “Jobs involving machinery, industrial sites, or construction usually aren’t covered by credit card insurance.”

Most policies exclude existing health issues or only cover emergency stabilisation. “Always declare conditions and check for extra coverage.”

Even trip disruptions may fall out of coverage, he says. “Delays, missed connections, cancellations due to weather, strikes, or airline issues are often not covered unless you buy a top-up.”

Top-ups are often necessary. “Extra coverage is usually needed for higher medical limits, adventure activities, or baggage and cancellation protection.

“Even short trips can become expensive if top-ups are not added to your credit card cover,” Feris says. “A hospital stay in the US or Europe can easily exceed N$500,000, and medical evacuation or repatriation can run into the millions,” explains Feris.

Ultimately, while credit card travel insurance can offer an initial layer of protection, Feris says that it is crucial to ensure you have a complete safety net.

“We all want peace-of-mind when travelling. Travellers who take the time to understand the exclusions, activation requirements, and coverage limits are far better positioned to protect themselves against unexpected losses and disruptions,” says Feris.

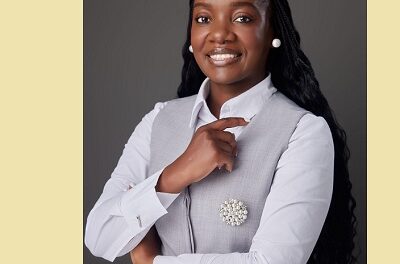

In the photo: Franco Feris, Chief Executive Officer at Santam Namibia Limited.

{kind=link}